Quick Summary

- Family health insurance in 2026 is not just about monthly premiums.

Deductibles, out-of-pocket limits, and provider networks can significantly change total annual cost.

- For many households, the most suitable plan depends on expected medical usage and risk tolerance.

- Comparing total yearly exposure rather than advertised pricing often leads to better decisions.

Why Health Insurance Works Differently for Families

Health coverage for families operates differently than individual plans.

Multiple dependents increase the likelihood of pediatric visits, prescriptions, and urgent care appointments. Even in healthy households, total medical interactions tend to be higher.

Because of this, deductible structure and cost-sharing rules matter more for families than for individuals.

A plan that appears inexpensive may become more costly once several family members begin using care.

The Four Cost Areas Families Should Review

1. Monthly Premium – Premiums are predictable and easy to compare. However, they represent only one part of total spending. Two plans with similar premiums may differ significantly in cost-sharing.

2. Family Deductible Structure – Many family plans include both:

- Individual deductibles

- A combined family deductible

Some plans activate broader coverage once the family total is reached. Others require each person to meet separate thresholds first.

Understanding this structure can clarify which plan may reduce financial surprises.

3. Out-of-Pocket Maximum – The out-of-pocket maximum limits total cost-sharing during the year.

For families, this number can influence financial stability in higher-usage scenarios.

Lower caps may provide greater protection during unexpected medical events.

4. Copays and Coinsurance – Routine care is common for families.

Some plans use fixed copays for visits. Others rely on percentage-based coinsurance after the deductible is met.

Predictability of these payments often influences long-term satisfaction.

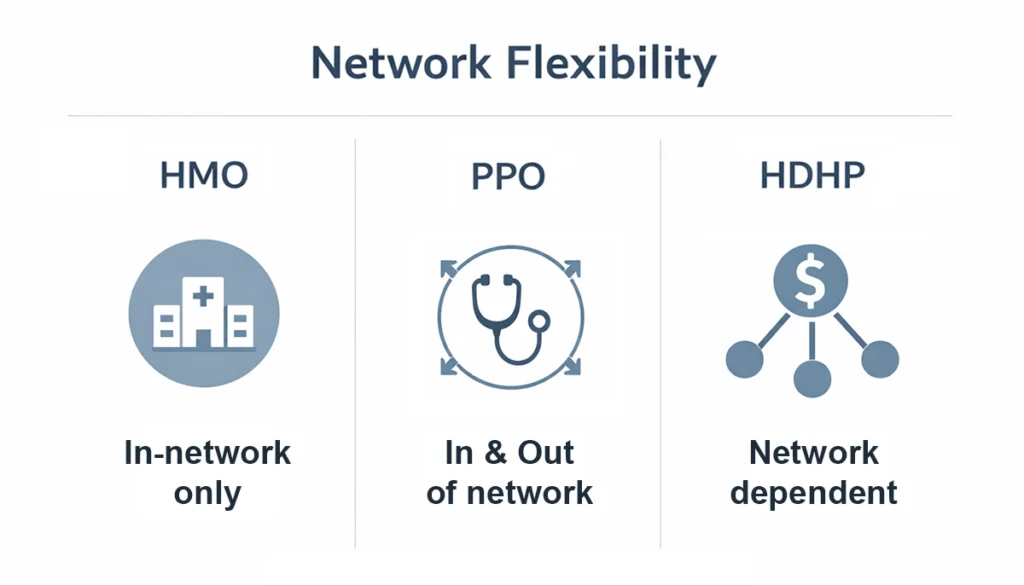

Comparing Common Plan Types in 2026

HMO Plans – HMO plans generally offer structured care within defined networks.

Premiums may be lower, but provider flexibility can be limited. Referrals are often required for specialists.

Families comfortable with coordinated primary care sometimes consider this model manageable.

PPO Plans – PPO plans usually provide broader provider networks.

Premiums may be higher, yet flexibility in choosing specialists can be valuable, particularly for children requiring specific care.

For some families, flexibility outweighs additional premium cost.

High-Deductible Health Plans (HDHP) – HDHPs tend to feature lower premiums and higher deductibles.

These plans are often paired with Health Savings Accounts (HSAs), which allow tax-advantaged savings for eligible expenses.

For families with low expected usage and sufficient savings, this structure may be practical. For households with frequent care needs, upfront expenses may be higher.

| Plan Type | Monthly Premium | Family Deductible | Out-of-Pocket Max |

|---|---|---|---|

| HMO | $1,800 | $4,000 | $9,000 |

| PPO | $2,050 | $3,000 | $8,000 |

| HDHP | $1,600 | $6,500 | $13,000 |

*Example cost structure for comparison purposes only. Illustrative example. Actual costs vary by state and provider.

How Family Size Influences Total Cost

Pricing may vary depending on:

- Number of dependents

- Age distribution

- Geographic location

- Employer-sponsored versus marketplace coverage

In some cases, adding additional children does not increase premiums proportionally beyond a certain tier.

Reviewing how dependents are categorized within each plan can clarify cost expectations.

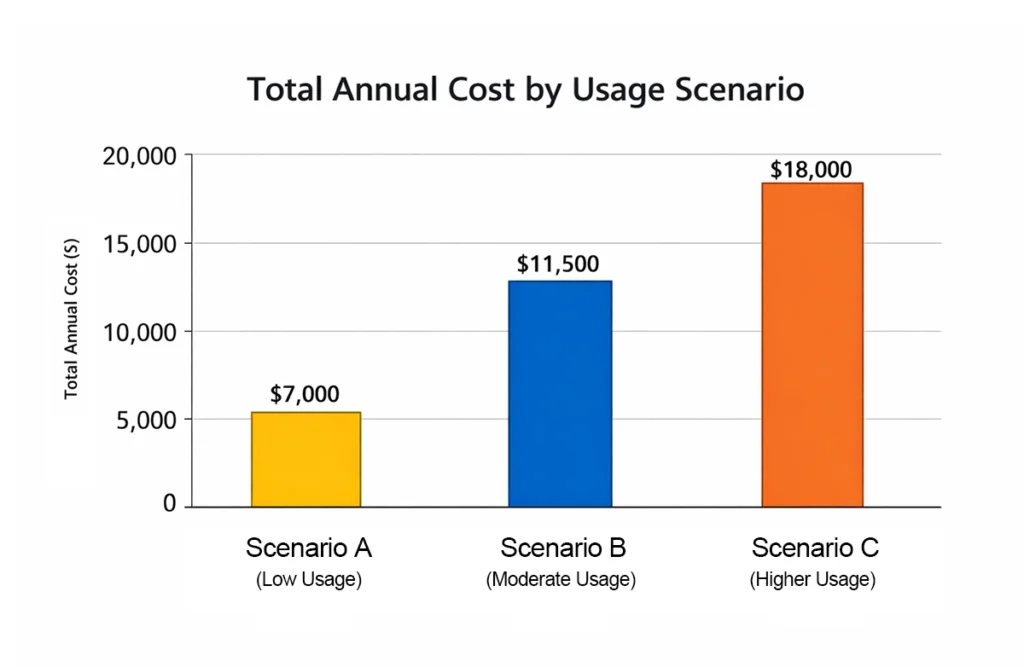

Evaluating Total Annual Exposure

Rather than focusing only on monthly premiums, many families evaluate potential total yearly spending under different scenarios:

- Low usage year (routine visits only)

- Moderate usage year (routine care plus prescriptions)

- Higher usage year (specialist visits or urgent events)

This approach highlights how deductibles and out-of-pocket limits affect overall financial exposure.

Actual costs vary based on provider contracts and individual circumstances.

Provider Network Considerations

Access to pediatricians, urgent care centers, and children’s hospitals often influences plan selection.

Before enrolling, families may review:

- In-network provider directories

- Prescription formularies

- Emergency care rules

Network limitations sometimes affect satisfaction more than pricing differences.

Common Comparison Mistakes

Families sometimes select plans based solely on the lowest premium.

Others rely on past coverage assumptions without reviewing updated plan documents.

Insurance offerings may change annually, including pricing, coverage design, and network participation.

Carefully reviewing structured details may reduce misunderstandings later.

2026 Market Considerations

Health insurance markets evolve over time.

Premium adjustments, insurer participation, and regulatory updates may affect plan availability.

Reviewing updated documents during each enrollment period can help ensure coverage aligns with current needs.

Final Thoughts

Health insurance comparison for families in 2026 is not about finding a universally “best” option.

It involves evaluating how coverage structure aligns with household usage patterns and financial priorities.

Premiums, deductibles, networks, and cost-sharing rules interact in ways that can significantly influence total annual cost.

*This content is provided for general educational purposes only and does not constitute insurance, financial, or legal advice. Coverage options and costs vary by individual circumstances, location, and insurer policies.