Quick Summary

If you’re self-employed in 2026, the best health insurance plan is rarely the one with the lowest premium. It’s the one that balances total yearly cost, provider access, and financial risk protection.

Most self-employed individuals typically compare:

- ACA Marketplace plans

- Off-Marketplace individual plans

- A spouse’s employer plan

- COBRA (short-term)

- High-Deductible Health Plans (HDHP) paired with an HSA

The right choice depends on three factors:

- Expected medical usage

- Network and specialist access

- Risk tolerance for out-of-pocket costs

*This guide provides a structured framework to help you evaluate your options confidently.

*Educational information only. Plan rules and availability vary by state and insurer.

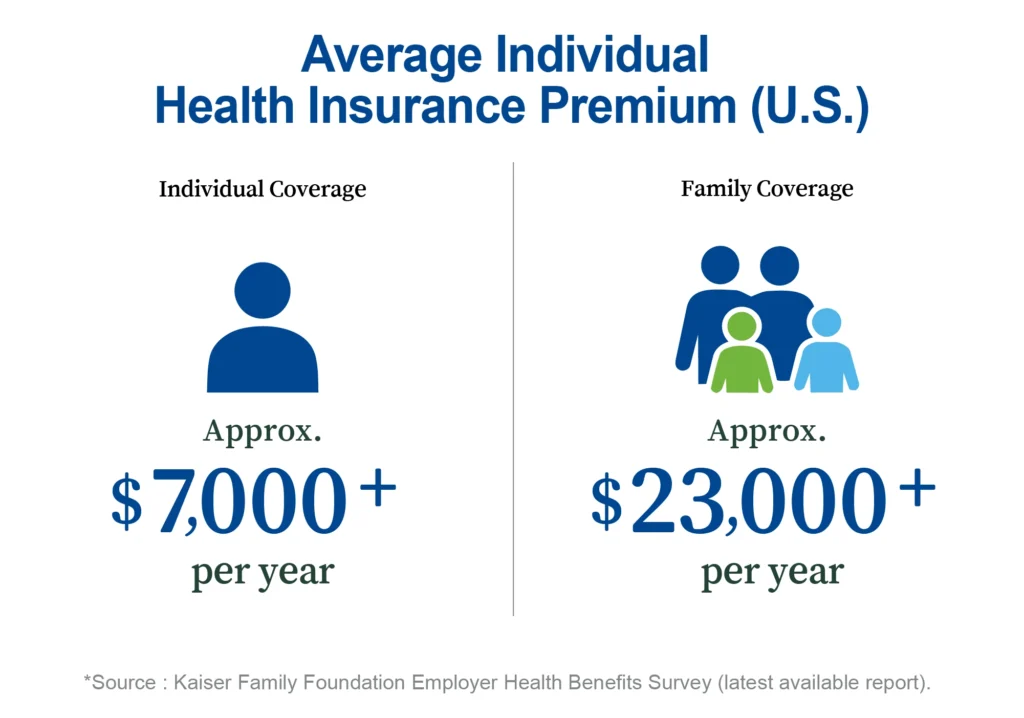

Why Health Insurance Is Different for the Self-Employed

Unlike traditional employees, self-employed individuals typically pay the full premium without employer contribution. That means plan design and total cost matter significantly more.

Key differences include:

- Full exposure to monthly premiums

- Greater sensitivity to deductibles and out-of-pocket maximums

- Income variability that may affect affordability planning

- Need for predictable cash-flow management

For freelancers, consultants, gig workers, and small business owners, insurance becomes a strategic budgeting decision — not just a compliance task.

Your Primary Coverage Paths in 2026

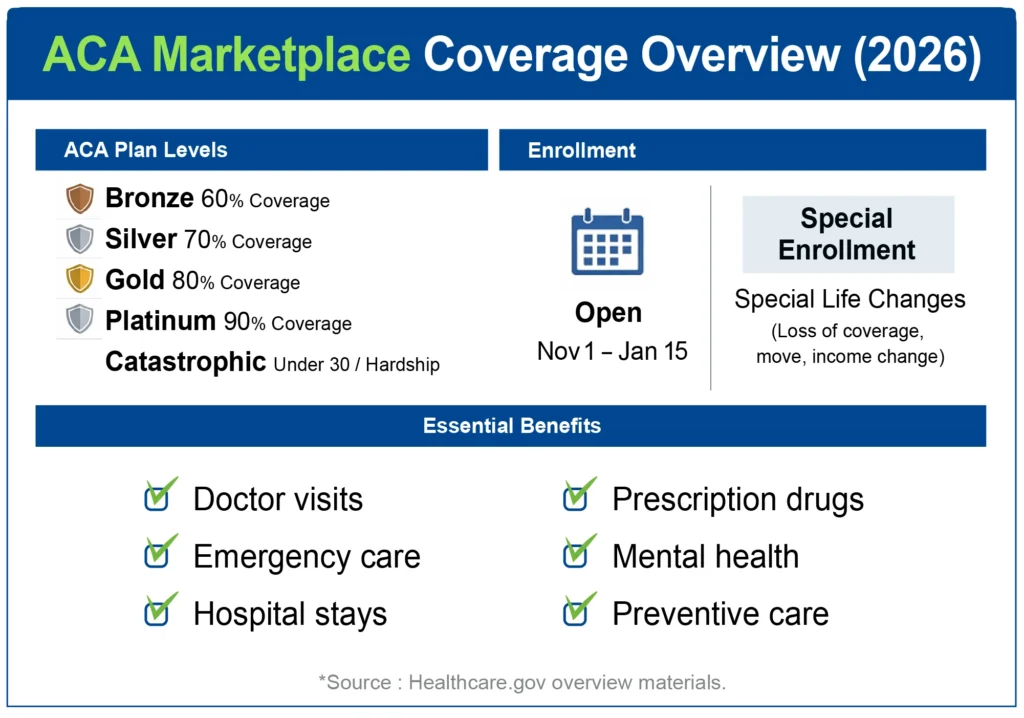

ACA Marketplace Plans

For many self-employed individuals, Marketplace plans serve as the default starting point.

Benefits include:

- Standardized plan categories

- Essential health benefit protections

- Structured comparison tools

- Clear enrollment windows

Considerations:

- Network limitations in some regions

- Referral requirements (often with HMO plans)

- Premium variation by location

Best suited for individuals who want structured plan comparisons and regulatory protections.

Off-Marketplace Individual Plans

Some insurers offer plans outside the Marketplace in select states.

Why consider them:

- Alternative network configurations

- Potentially different plan structures

However, these plans require careful review of benefits, networks, and exclusions.

Spouse or Partner Employer Coverage

If accessible, joining a spouse’s employer plan can provide:

- Potential employer premium contribution

- Broad networks

- Simplified administration

This option may offer stability, but dependent premiums should be reviewed carefully.

COBRA (Short-Term Continuity)

COBRA may allow you to continue your prior employer coverage temporarily.

Advantages:

- Keeps current doctors and treatment plans

- No network disruption

Trade-off:

- Often higher premiums

Typically best as a transition solution rather than long-term strategy.

HDHP + HSA Strategy

High-Deductible Health Plans paired with a Health Savings Account can be suitable for:

- Low-to-moderate healthcare usage

- Individuals with strong emergency savings

- Long-term planning approach to healthcare expenses

The trade-off is higher upfront cost exposure before coverage intensifies.

Understanding Plan Types: HMO vs PPO vs EPO vs HDHP

| Plan Type | Avg Monthly Premium | Deductible | Out-of-Pocket Max | Best For |

|---|---|---|---|---|

| HMO | $420 | $3,000 | $8,500 | Moderate usage |

| PPO | $480 | $2,000 | $7,500 | Specialist flexibility |

| EPO | $410 | $3,500 | $8,200 | In-network flexibility |

| HDHP | $350 | $6,500 | $8,000 | Low usage + savings |

HMO Plans

- Lower premiums in many cases

- Primary care coordination required

- Referral system for specialists

Suitable for those comfortable staying within a managed network.

PPO Plans

- More provider flexibility

- Often higher premiums

- Some out-of-network coverage

Preferred by individuals who prioritize specialist access and flexibility.

EPO Plans

- In-network only

- No referral requirement in many cases

- Balanced cost structure

Useful for those who want flexibility without out-of-network use.

HDHP Plans

- Higher deductible threshold

- Often compatible with HSA

- Lower premium, higher early-year exposure

Best evaluated alongside savings capacity.

The 7 Metrics That Matter Most

When comparing plans, focus on:

- Monthly premium

- Individual deductible

- Family deductible (if applicable)

- Out-of-pocket maximum

- Specialist copays

- Coinsurance percentage

- Prescription drug tiers

Premium alone does not determine affordability. Total annual exposure matters more.

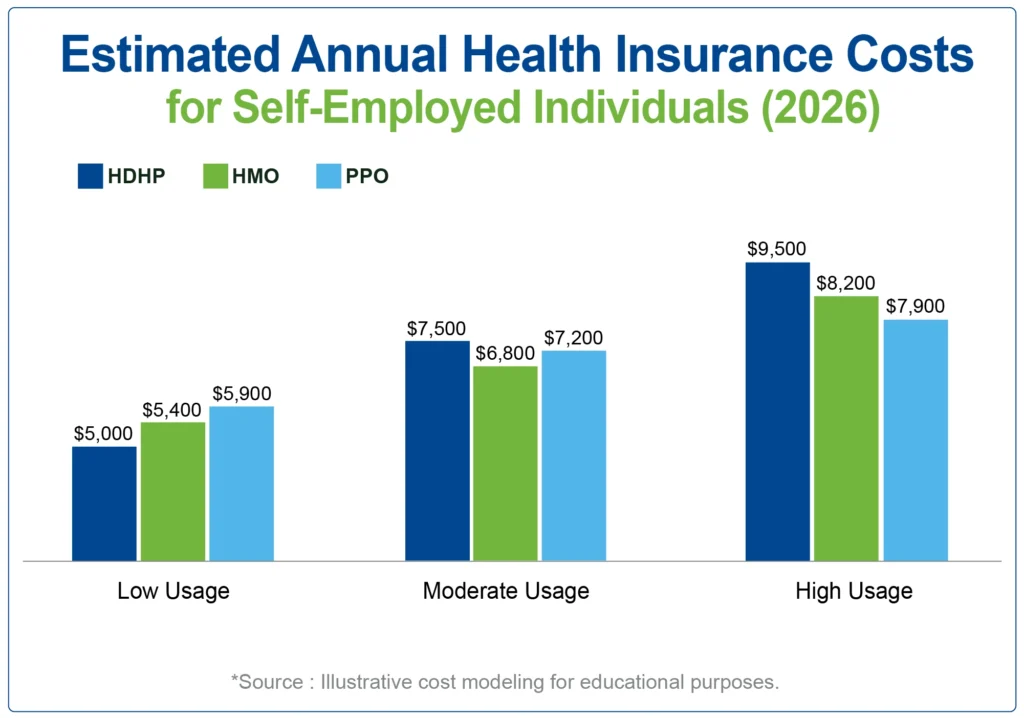

Cost Modeling: Low, Moderate, and High Usage Scenarios

Low Usage Scenario

- Preventive visits only

- Few prescriptions

- Minimal specialist care

In this scenario, lower premiums and HSA-compatible plans may provide value.

Moderate Usage Scenario

- Regular doctor visits

- Prescriptions

- Occasional urgent care

Mid-tier plans with predictable copays may reduce budgeting stress.

High Usage Scenario

- Ongoing specialist care

- Planned procedures

- Higher prescription needs

Lower out-of-pocket maximums become critical.

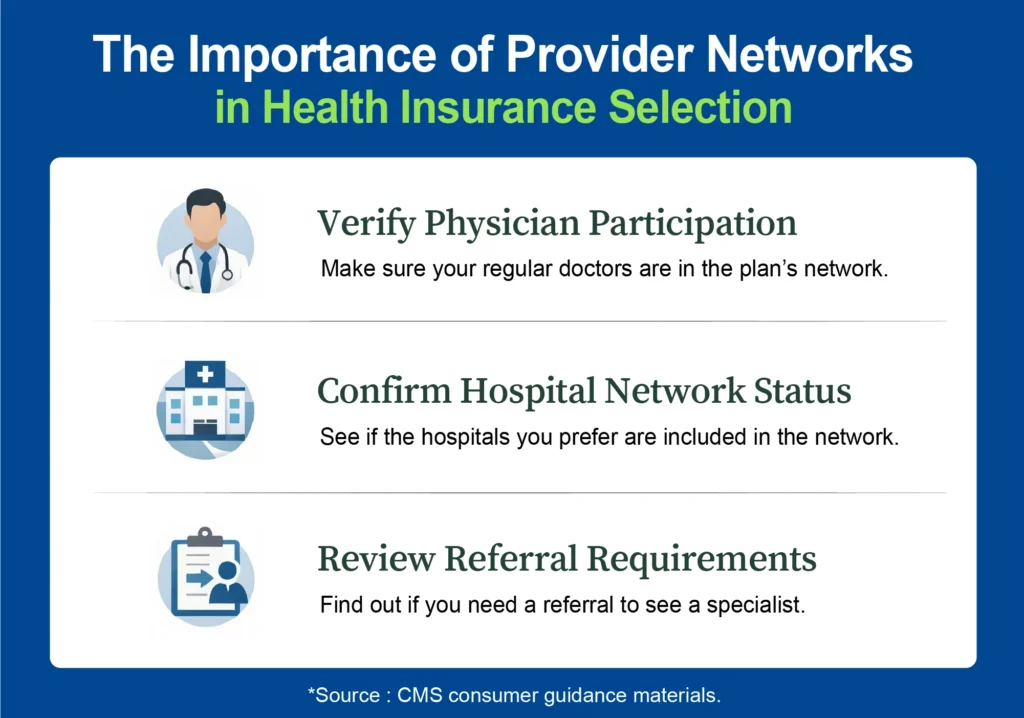

Provider Networks: The Often Overlooked Factor

Before enrolling:

- Confirm your primary physician is in-network

- Verify specialist inclusion

- Check hospital participation

- Review telehealth availability

Network disruption can outweigh premium savings.

Always verify directly when possible.

Prescription Coverage and Formulary Review

Prescription tiers significantly affect total cost.

Consider:

- Generic vs brand pricing

- Specialty medication tiers

- Prior authorization requirements

A slightly higher premium plan may reduce prescription expense volatility.

Risk Tolerance and Financial Planning

Self-employed individuals should define:

- Maximum acceptable annual exposure

- Cash-flow stability

- Emergency reserve level

Plans with higher deductibles require stronger reserves.

Common Mistakes Self-Employed Individuals Make

- Selecting based on premium only

- Ignoring out-of-pocket maximum

- Assuming provider network without verification

- Overlooking prescription tier rules

- Failing to estimate annual exposure

Structured comparison reduces these risks.

A Step-by-Step Decision Framework

Step 1: Identify Non-Negotiables

List required doctors, hospitals, medications.

Step 2: Define Risk Ceiling

Determine your financial comfort zone for worst-case year.

Step 3: Compare Three Plans Side-by-Side

Use consistent metrics across options.

Step 4: Model Annual Costs

Estimate:

- Premium total

- Deductible usage

- Copays

- Prescription costs

Step 5: Validate Network and Enrollment Rules

Reconfirm network status before final enrollment.

When a Higher Premium May Be Smarter

Higher premiums sometimes reduce overall financial risk.

If you expect:

- Frequent care

- Ongoing specialist visits

- Family coverage

A lower deductible plan may reduce stress and unpredictability.

Special Considerations for Freelancers and Gig Workers

Irregular income increases importance of:

- Predictable copays

- Reasonable out-of-pocket maximum

- Stable network access

Budget stability often outweighs chasing the lowest premium.

Final Recommendation Framework

There is no universal “best” health insurance for the self-employed in 2026.

However, a practical rule of thumb:

- Low usage + savings buffer → consider HDHP

- Moderate usage → balanced mid-tier plan

- High usage or chronic conditions → prioritize lower out-of-pocket max

Always verify:

- Provider network

- Prescription formulary

- Annual exposure estimate

Insurance should protect your long-term financial stability — not introduce uncertainty.

Frequently Asked Questions

What is the best health insurance option for self-employed individuals in 2026?

The best option depends on usage patterns, provider needs, and financial risk tolerance rather than premium alone.

Is HDHP always cheaper?

Not necessarily. Lower premiums may be offset by higher out-of-pocket exposure.

Should freelancers prioritize PPO plans?

PPO plans provide flexibility but may carry higher premiums. Evaluate based on network needs and specialist access.

How can I compare plans effectively?

Use a consistent comparison model including premium, deductible, out-of-pocket maximum, copays, prescriptions, and network validation.

Conclusion: Choosing the Right Health Insurance as a Self-Employed Professional in 2026

Selecting health insurance as a self-employed individual in 2026 requires more than comparing premiums. The most effective approach is to evaluatetotal annual exposure, provider access, prescription coverage, and your personal risk tolerance.

For low healthcare usage, high-deductible plans paired with disciplined savings may offer flexibility. For moderate usage, balanced plans with predictable copays can reduce budgeting uncertainty. For higher medical needs, plans with lower out-of-pocket maximums and strong networks often provide greater financial protection.

No single plan is universally “best.” The right choice depends on your expected usage pattern, income stability, and access to preferred providers.

Before enrolling, confirm:

- Network participation for your doctors and hospitals

- Prescription coverage details

- Deductible and out-of-pocket limits

- Enrollment timing and plan rules

A structured comparison approach will typically produce better long-term outcomes than choosing based on premium alone.

*Educational information only. Coverage terms and eligibility vary by state and insurer.