Buying car insurance as a young driver can feel overwhelming. Premiums are often significantly higher than average, and the range of policy options makes comparison difficult. A proper auto insurance comparison for young drivers should not focus only on monthly cost. It should evaluate how coverage limits, deductibles, and risk factors influence the real financial protection a policy provides.

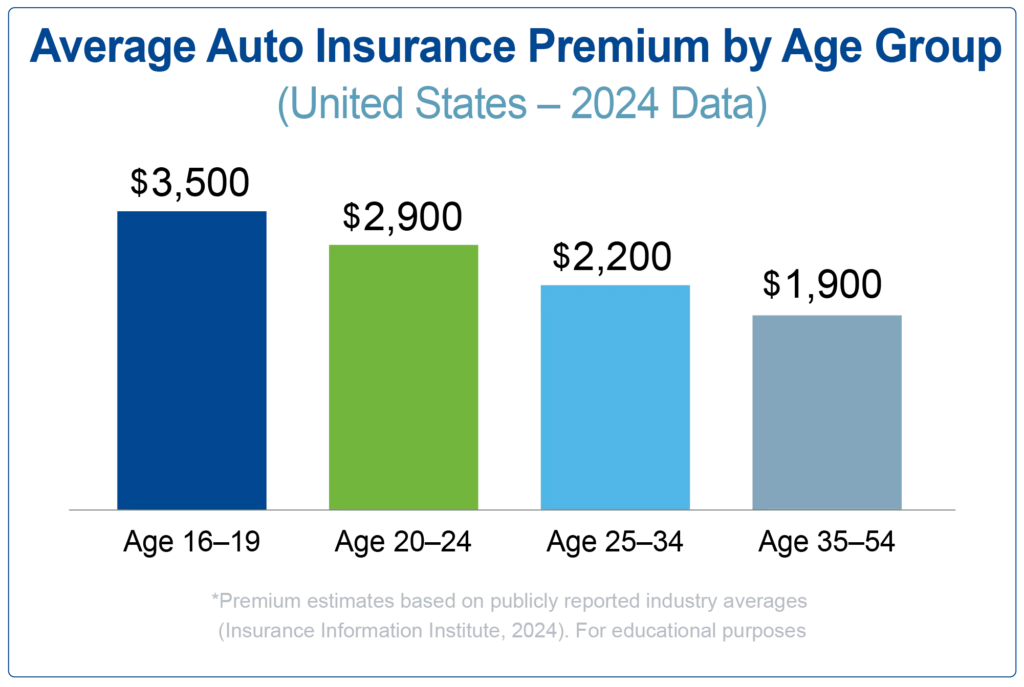

Young drivers typically face higher premiums because insurers evaluate risk based on driving experience, accident probability, and statistical claim data. According to the Insurance Information Institute, drivers under age 25 represent a smaller share of drivers but are involved in a disproportionately higher percentage of accidents. Because of this, insurers price policies conservatively.

However, higher premiums do not mean young drivers cannot find reasonable coverage. The key is understanding how different policy components interact. When comparing policies, focus on coverage structure, deductible strategy, and total yearly exposure rather than only looking at monthly payments.

Quick Summary: What Young Drivers Should Compare First

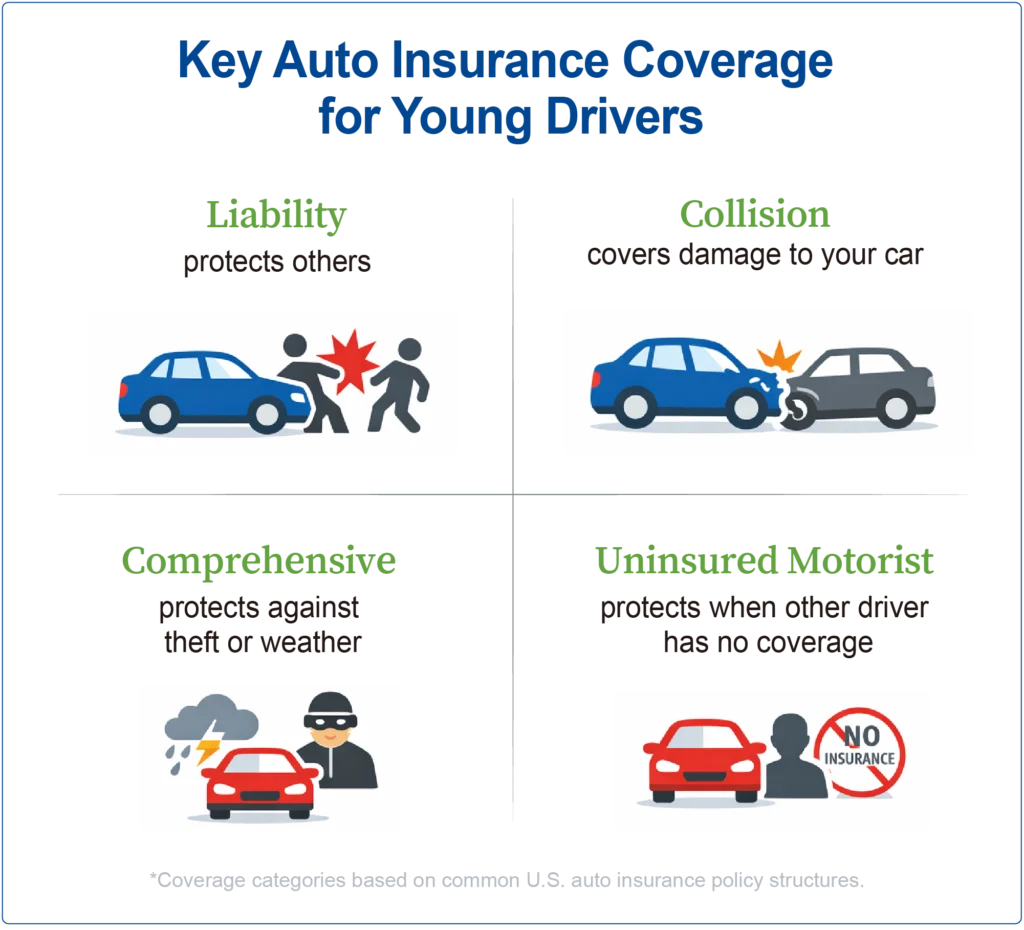

Comparison of key auto insurance coverages for young drivers including liability, collision, comprehensive, and uninsured motorist protection.

Before diving into policy details, it helps to understand the most important variables affecting premiums.

A clear auto insurance comparison for young drivers should evaluate:

- Liability coverage limits

- Collision and comprehensive protection

- Deductible levels

- Discount eligibility

- Total annual premium

Young drivers often save money by adjusting deductibles, qualifying for good student discounts, or joining family policies. But the cheapest option is not always the safest one financially. The goal is to balance affordability with protection.

Why Auto Insurance Costs Are Higher for Young Drivers

Insurance companies use actuarial data to estimate risk. Younger drivers, particularly those between 16 and 24, statistically experience higher accident rates than older drivers.

Several factors influence this risk calculation:

Limited Driving Experience

Buying car insurance as a young driver can feel overwhelming. Premiums are often significantly higher than average, and the range of policy options makes comparison difficult. A proper auto insurance comparison for young drivers should not focus only on monthly cost. It should evaluate how coverage limits, deductibles, and risk factors influence the real financial protection a policy provides.

Accident Statistics

Government traffic safety studies show that drivers under 25 are more likely to be involved in collisions compared to middle-aged drivers. Even small incidents can increase insurance costs.

Risk Exposure

Young drivers often drive older vehicles, commute frequently, or drive during higher-risk hours. These patterns affect underwriting decisions.

Understanding these factors helps explain why performing a thoughtful auto insurance comparison for young drivers is especially important.

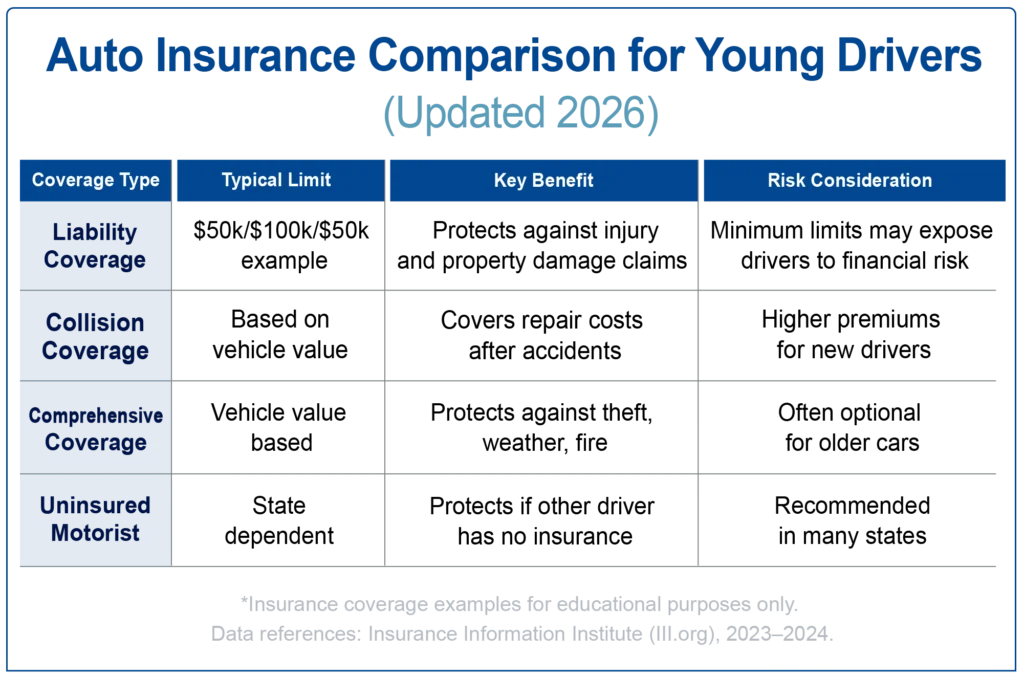

Core Coverage Types Young Drivers Must Compare

Car insurance policies are built from several coverage components. Each plays a different role in protecting drivers financially.

Liability Coverage

Liability coverage protects against damage or injuries caused to others during an accident.

Typical liability coverage limits include:

- $50,000 per person for bodily injury

- $100,000 per accident

- $50,000 property damage

Many financial planners recommend higher limits when possible. Although minimum state requirements are lower, higher liability protection reduces long-term financial risk.

Collision Coverage

Collision insurance pays for repairs to your own vehicle after an accident, regardless of fault.

Young drivers often choose collision coverage when:

- The car is financed

- The vehicle still has meaningful value

- Repair costs could exceed emergency savings

Comprehensive Coverage

Comprehensive insurance protects against non-collision risks such as:

- Theft

- Weather damage

- Fire

- Falling objects

For newer vehicles, comprehensive coverage can provide important financial protection.

Uninsured Motorist Coverage

This coverage protects drivers if the at-fault driver has no insurance or insufficient coverage. In many states, this protection is strongly recommended.

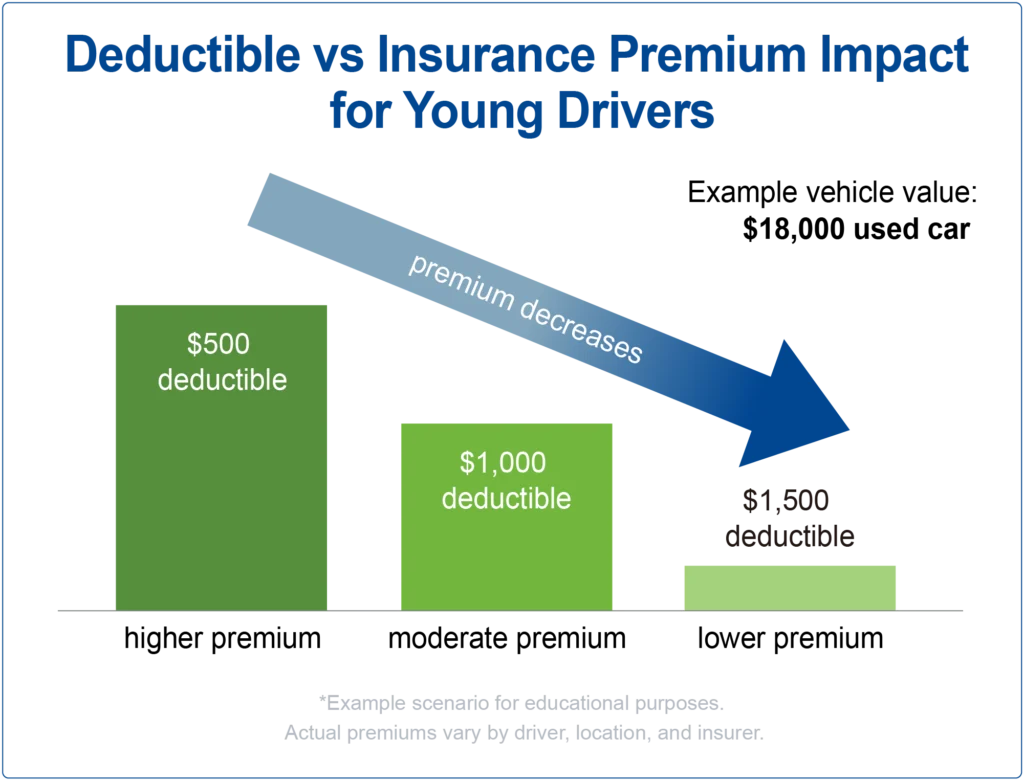

Deductible Strategy and Premium Trade-Offs

A deductible is the amount you pay before insurance coverage begins. Deductibles influence premiums significantly.

Typical deductible levels include:

- $500

- $1,000

- $1,500

Higher deductibles generally reduce premiums. However, they increase the amount you must pay out-of-pocket after an accident.

Young drivers often choose a moderate deductible that balances affordability with manageable financial exposure.

For example:

A $1,000 deductible may lower premiums compared to a $500 deductible, but drivers must be confident they could afford the higher cost if a claim occurs.

Comparing Policy Structures for Young Drivers

When performing an auto insurance comparison for young drivers, it helps to analyze policy options using structured categories.

Key comparison points include:

- Monthly premium

- Deductible level

- Liability coverage limits

- Discount eligibility

- Vehicle value considerations

A comparison table inserted here can help readers visualize differences between policy structures.

This is also an ideal section to add a coverage comparison chart or policy comparison table to increase reader engagement and clarity.

Realistic Cost Scenarios for Young Drivers

Insurance premiums vary depending on driver profile, location, and vehicle type. Considering realistic scenarios can help illustrate cost differences.

Scenario 1: College Student Driver

A college student driving a used sedan with moderate mileage may prioritize affordability. Higher deductibles combined with safe-driving discounts could lower premiums.

Scenario 2: First-Time Driver with New Vehicle

If the car is financed, lenders usually require collision and comprehensive coverage. This increases premiums but ensures the vehicle is protected.

Scenario 3: Young Driver on Family Policy

Many insurers allow young drivers to join a parent’s policy. This often results in lower premiums compared to purchasing an individual policy.

These examples highlight why an informed auto insurance comparison for young drivers should consider personal circumstances.

Factors That Affect Premium Differences

Insurance companies use multiple variables to calculate premiums.

Important factors include:

- Driver age

- Driving record

- Vehicle type

- Annual mileage

- Location

- Credit-based insurance score (in some states)

Drivers can influence some of these variables over time. Maintaining a clean driving record is one of the most effective ways to reduce insurance costs.

Discounts Young Drivers Should Look For

Many insurers offer discounts that significantly reduce premiums.

Common discounts include:

Good Student Discount

Students with strong academic performance may qualify for reduced premiums.

Defensive Driving Course

Completing an approved driver safety course can demonstrate lower risk.

Telematics Programs

Usage-based insurance programs monitor driving behavior and reward safe driving habits.

Multi-Policy Discounts

Bundling auto insurance with renters or homeowners insurance may reduce overall costs.

These opportunities are important when conducting a full auto insurance comparison for young drivers.

Common Mistakes Young Drivers Make When Buying Insurance

Several mistakes frequently lead to higher costs or insufficient coverage.

Common issues include:

- Choosing minimum liability limits

- Ignoring deductible impact

- Focusing only on premium price

- Skipping uninsured motorist protection

- Failing to compare multiple insurers

Insurance decisions should be evaluated carefully to avoid long-term financial risk.

Frequently Asked Questions

Why do young drivers pay higher car insurance premiums?

Young drivers statistically have higher accident rates, which increases risk for insurers. Premiums usually decrease as drivers gain experience and maintain safe driving records.

How can young drivers reduce insurance costs?

Drivers can reduce premiums by maintaining safe driving habits, qualifying for student discounts, increasing deductibles, or joining a family policy.

Is minimum coverage enough for young drivers?

Minimum coverage satisfies legal requirements but may not provide adequate financial protection after a serious accident.

Conclusion

Choosing the right policy requires more than selecting the cheapest option. A thoughtful auto insurance comparison for young drivers should consider coverage structure, deductible strategy, and total financial risk.

Young drivers benefit most from evaluating policies carefully and understanding how coverage types interact. Liability protection, collision coverage, and deductibles all influence long-term costs.

By comparing policy features, evaluating discounts, and considering realistic driving scenarios, young drivers can find insurance that balances affordability with meaningful financial protection.

Car insurance is ultimately about risk management. The most effective policy is one that protects both your vehicle and your financial stability over time.