Quick Summary: Home Insurance Coverage Comparison for New Homeowners

Buying your first home comes with one unavoidable decision: choosing the right policy. A proper home insurance coverage comparison for new homeowners goes far beyond looking at premiums. The most important factors are:

- Dwelling coverage limits

- Deductible structure

- Liability protection

- Replacement cost vs. actual cash value

- Total annual exposure

New homeowners often underestimate risk. The goal is not the cheapest policy — it’s financial protection aligned with your property value and risk profile.

Why Home Insurance Coverage Comparison Matters in 2026

The housing market has shifted. Construction costs, rebuilding expenses, and climate-related risks have increased in many U.S. states.

For new homeowners, this creates three risks:

- Underinsuring the dwelling

- Choosing deductibles that strain emergency savings

- Ignoring liability exposure

A structured home insurance coverage comparison for new homeowners reduces these mistakes.

Core Coverage Types New Homeowners Must Compare

| Coverage Type | Typical Limit | Key Risk | Upgrade Option |

|---|---|---|---|

| Dwelling Coverage | Based on rebuild cost (e.g., $350,000 example) | Underinsurance risk | Extended replacement cost endorsement |

| Other Structures | Typically 10% of dwelling | Detached structure loss | Increased percentage rider |

| Personal Property | 50–70% of dwelling | Depreciation risk | Replacement cost coverage |

| Liability Protection | $100,000–$500,000 typical | Lawsuit exposure | Umbrella policy |

| Additional Living Expenses | 20–30% of dwelling | Temporary housing costs | Extended ALE rider |

National average homeowners insurance premium: $1,428 per year (Insurance Information Institute, 2023).

For educational purpose only.

1. Dwelling Coverage (Coverage A)

This protects the physical structure of your home.

Compare:

- Policy limit vs. rebuild cost

- Extended replacement cost options

- Inflation guard riders

Many first-time buyers use the purchase price instead of the rebuilding cost. These numbers are not always the same.

2. Other Structures Coverage

Covers detached garages, fences, sheds.

Usually calculated as a percentage of dwelling coverage (often 10%).

If you have a detached structure, verify limits during your home insurance coverage comparison for new homeowners.

3. Personal Property Coverage

Covers belongings inside the home.

Key comparison factors:

- Replacement cost vs actual cash value

- Sub-limits for jewelry, electronics, collectibles

- Off-premises coverage

Replacement cost is generally more protective but may increase premiums.

4. Liability Protection

Liability covers injuries or property damage to others.

Typical limits:

- $100,000

- $300,000

- $500,000+

For new homeowners, higher liability limits often provide stronger long-term protection, especially if assets are growing.

5. Additional Living Expenses (ALE)

If your home becomes uninhabitable, ALE covers temporary housing costs.

Compare:

- Covered causes of loss

- Time limits

- Percentage limits

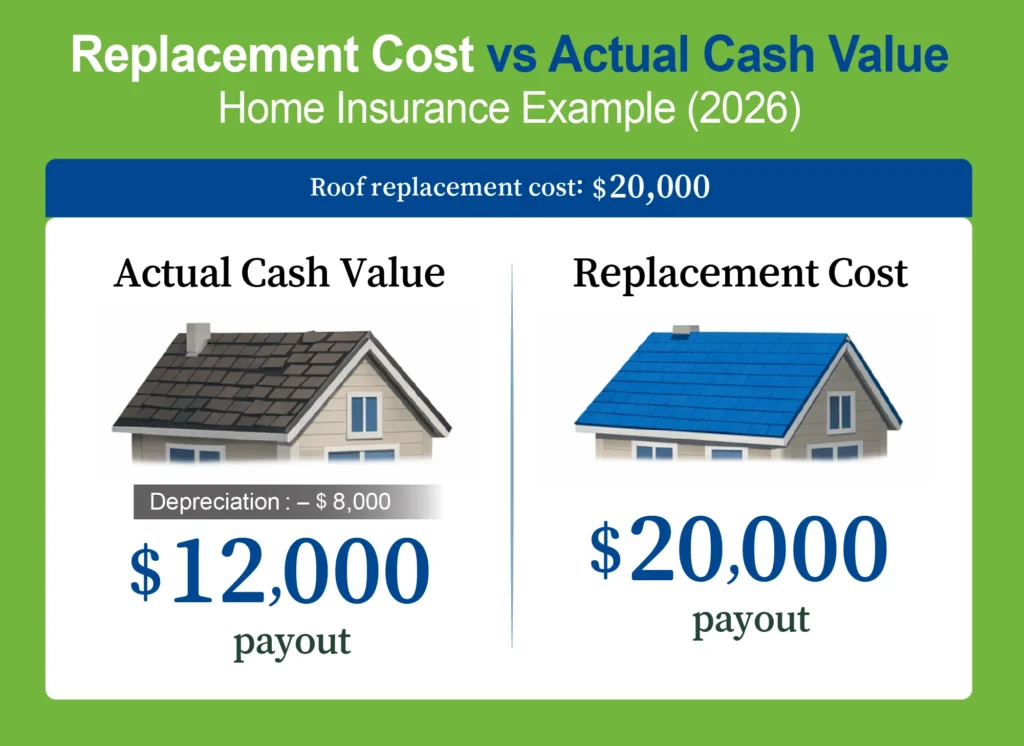

Replacement Cost vs Actual Cash Value: A Critical Comparison

A proper home insurance coverage comparison for new homeowners must evaluate valuation methods.

Replacement Cost:

- Pays to rebuild or replace without depreciation deduction.

Actual Cash Value:

- Deducts depreciation before payout.

In many cases, replacement cost provides more predictable financial recovery.

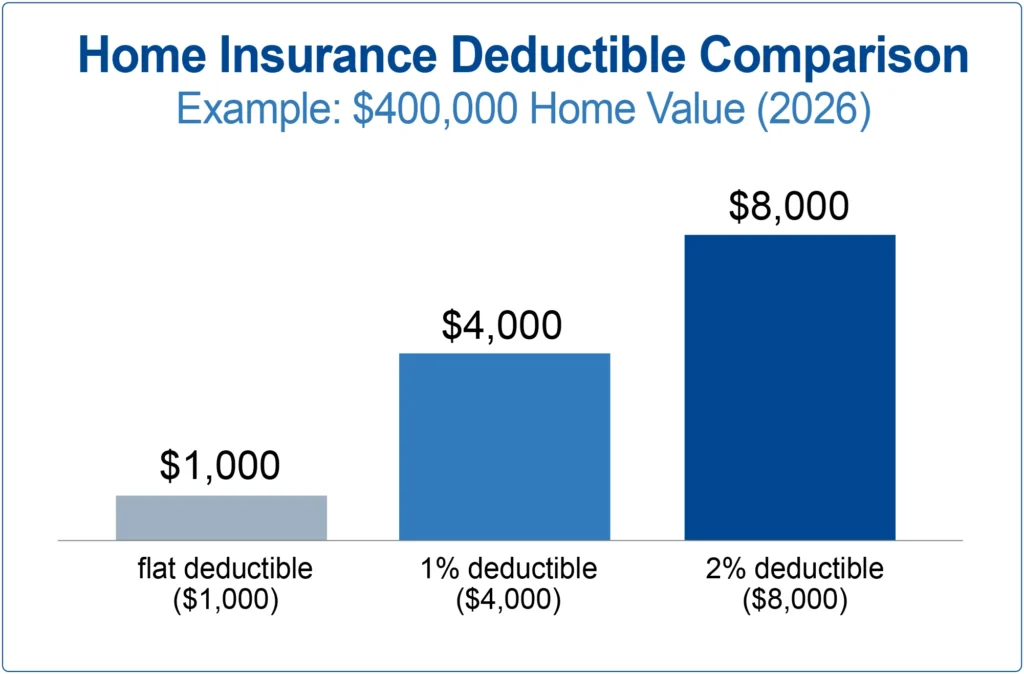

Deductible Strategy and Risk Modeling

eductibles directly impact premiums and out-of-pocket exposure.

Common deductible levels:

- $500

- $1,000

- $2,500

- Percentage-based (1%–2% of dwelling value)

Example scenario:

$400,000 dwelling

1% deductible = $4,000 out-of-pocket

New homeowners should align deductibles with emergency savings capacity.

Home Insurance Coverage Comparison Table

Include columns such as:

- Coverage Type

- Standard Limit

- Upgrade Options

- Risk Consideration

- Best For

This visual will increase dwell time and clarity.

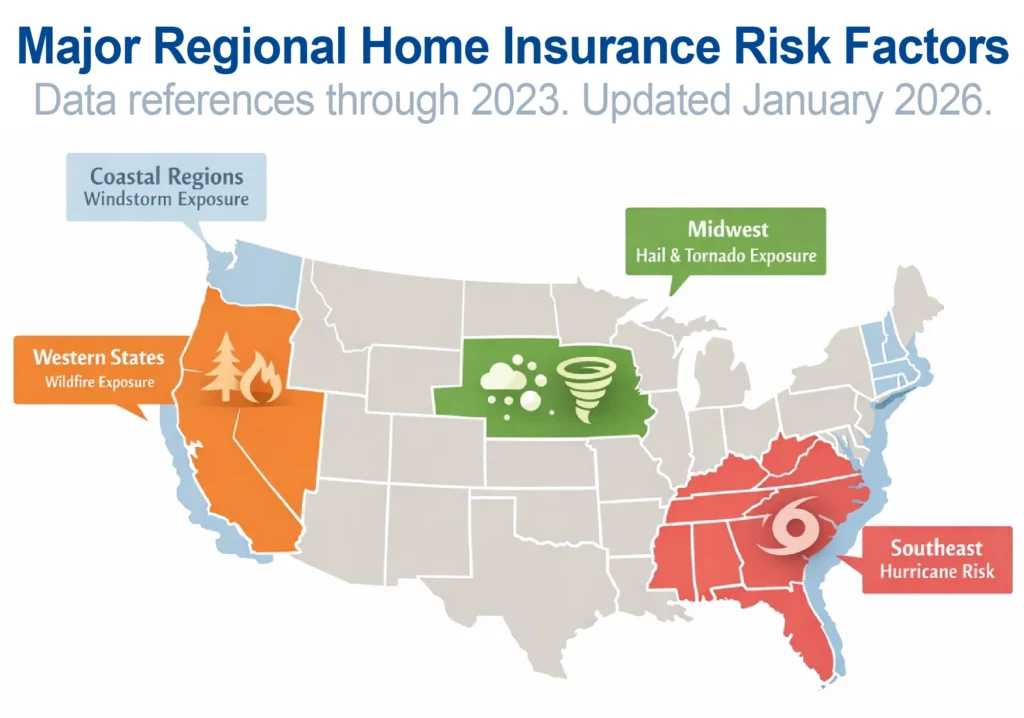

Regional Risk Considerations in the U.S.

Risk patterns based on publicly available FEMA and NOAA data through 2023. For educational purposes only.

Home insurance premiums and requirements vary by:

- State

- Weather exposure

- Local building costs

- Claims history

For example:

- Coastal states may include windstorm deductibles.

- Western states may have wildfire-related endorsements.

- Midwest regions may emphasize hail coverage.

Always verify state-specific requirements when conducting a home insurance coverage comparison for new homeowners.

Common Mistakes New Homeowners Make

- Choosing lowest premium without comparing coverage limits

- Underestimating rebuild cost

- Ignoring policy exclusions

- Not reviewing liability limits

- Skipping endorsement options

A structured comparison prevents reactive decisions.

Cost Factors That Impact Premiums

Premiums are influenced by:

- Home age

- Construction materials

- Roof condition

- Credit-based insurance scores (in many states)

- Claims history

- Deductible selection

Understanding these variables improves your home insurance coverage comparison for new homeowners.

Realistic Scenario Modeling

Scenario A: Low Risk Property

- New construction

- Suburban location

- Minimal claims history

Likely outcome:

Lower premium, moderate deductible flexibility.

Scenario B: Higher Exposure Property

- Older home

- Coastal location

- Higher rebuild cost

Likely outcome:

Higher premium, stricter deductible requirements.

Decision Framework for New Homeowners

When finalizing a policy:

- Confirm dwelling coverage equals estimated rebuild cost.

- Choose deductible aligned with emergency reserves.

- Increase liability limits if financially feasible.

- Review replacement cost options.

- Confirm exclusions and endorsements.

A methodical approach improves financial resilience.

Frequently Asked Questions

How much home insurance do new homeowners need?

Coverage should reflect rebuilding cost, not purchase price. Consult local construction cost estimates.

Is higher deductible always better?

Not necessarily. Higher deductibles reduce premiums but increase immediate financial exposure.

Should new homeowners choose replacement cost coverage?

Should new homeowners choose replacement cost coverage?

What affects home insurance premiums most?

Location, rebuild cost, deductible level, and claims history are primary factors.

Conclusion

A proper home insurance coverage comparison for new homeowners is a financial protection strategy — not just a shopping exercise.

The strongest policies balance:

- Adequate dwelling limits

- Sustainable deductibles

- Sufficient liability protection

- Realistic replacement cost coverage

New homeowners benefit most from evaluating total risk exposure rather than focusing solely on price.

*This guide is for informational purposes only. Coverage terms, eligibility, and availability vary by state and insurer. Always review policy documents carefully before enrollment.